AbbVie to Acquire Apogee

Paragon's long-acting atopic dermatitis & asthma pipeline pays off

Disclaimer: This newsletter is for educational and informational purposes only and does not constitute medical, investment, or financial advice, nor does it establish a provider-patient relationship. Content may include forward-looking statements and discussions of investigational therapeutic candidates that are not FDA/EMA approved; their safety and efficacy remain unestablished and clinical outcomes are unpredictable. While we strive for accuracy, all information is provided as is without guarantees. This newsletter is independent, and the author holds no financial positions in the companies mentioned nor receives third-party compensation for this coverage. Please find a complete version of our disclaimers at the bottom of this article and on our About page.

Introduction

On June 22, 2026, AbbVie announced a definitive agreement on an all-cash acquisition of Apogee Therapeutics for a total value of approximately $10.9 billion (AbbVie press release, AbbVie slide deck, Apogee press release). This acquisition centers on Apogee’s “diverse pipeline of multiple clinical-stage candidates in development across inflammatory and immunological diseases”:

Zumilokibart: Their lead program is a subcutaneous, half-life-extended mAb targeting IL-13 (a core driver of Type 2 inflammation) with maintenance dosing intervals of every 3 to 6 months (quarterly or twice-yearly). AbbVie/Apogee plans to start a Phase 3 atopic dermatitis trial in late 2026.

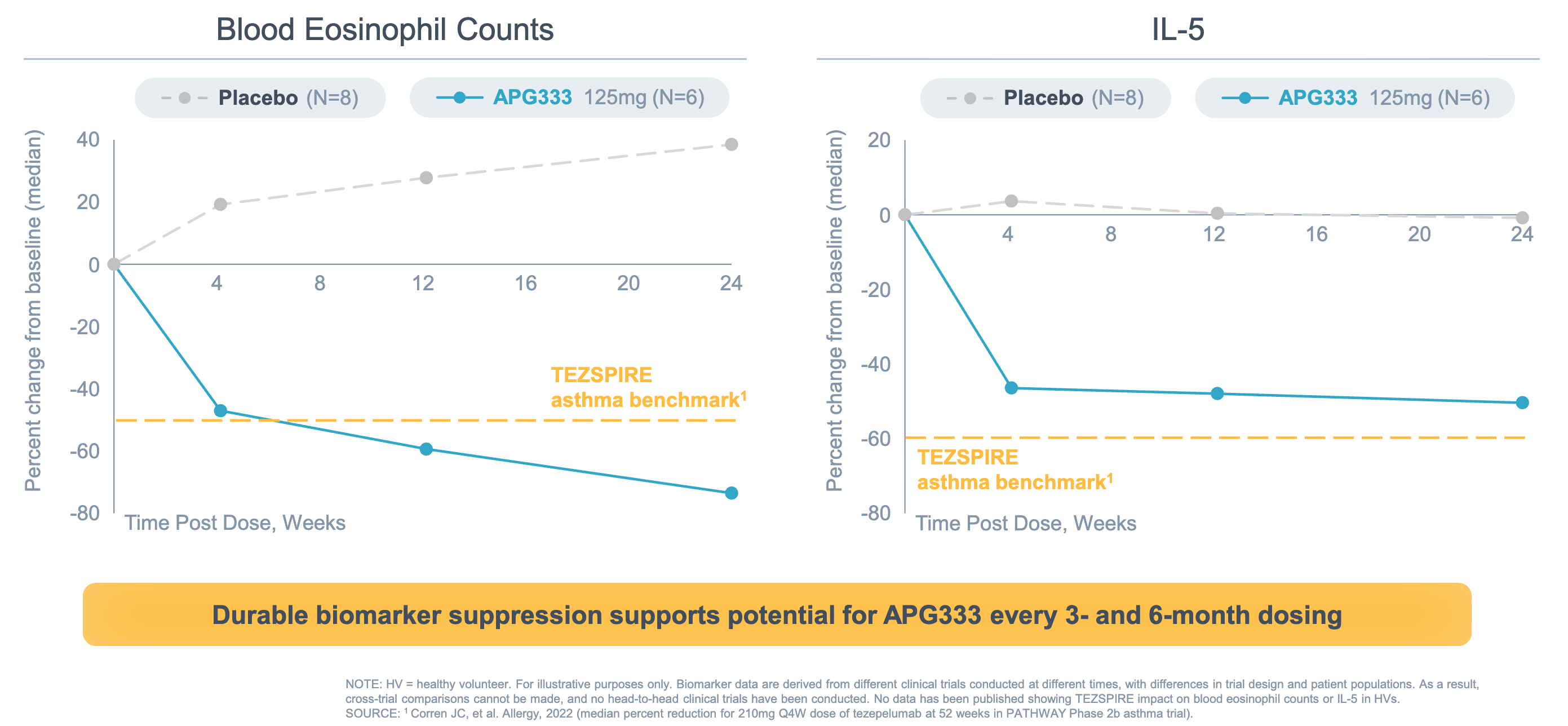

APG273: This is a fixed-dose combination of zumilokibart (anti-IL-13) + APG333 (an extended half-life anti-TSLP mAb). While the combination asset itself is in early stages, its components have demonstrated clinical activity in completed trials. In addition to zumilokibart’s positive Phase 1b asthma data, APG333 completed a Phase 1 trial confirming a long half-life in healthy volunteers and the ability to suppress relevant Type 2 inflammatory biomarkers for up to six months after a single dose.

APG279: This is a fixed-dose combination of zumilokibart (anti-IL-13) + APG990 (an extended half-life anti-OX40L mAb). A Phase 1b head-to-head study comparing APG279 directly against standard-of-care Dupixent in AD is fully enrolled and data are anticipated in late 2026.

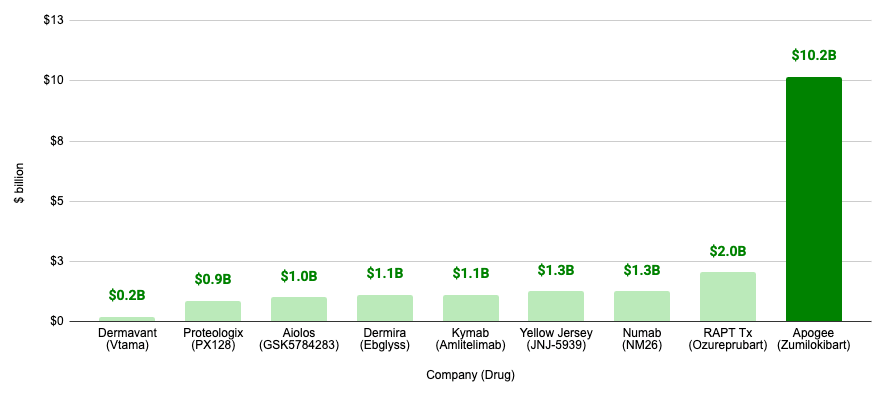

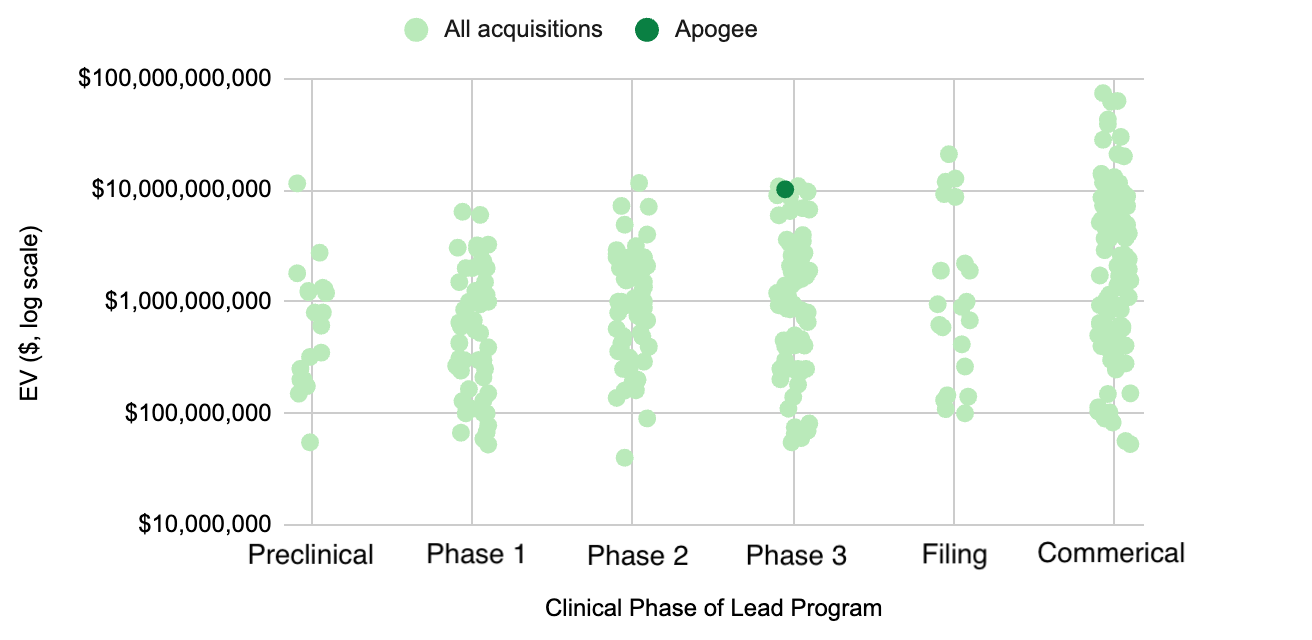

The $10.9 billion price tag of Apogee is unusually large. In fact, it is by far the largest acquisition in the atopic dermatitis and asthma spaces (first graph below), and is almost four-fold larger than the average acquisition with a lead asset in Phase 3 (see below).

In this article, we will focus on unpacking the M&A strategy that AbbVie highlighted in their presentation, finding out why Apogee’s high price tag is justified, and exploring the corporate history of Apogee.

We plan to discuss the cutting edge of atopic dermatitis and allergy in future Frontiers in Medicine pieces.

A Peek Into AbbVie’s M&A Strategy

AbbVie has spent over two decades building a pipeline of blockbuster medicines in immunology. Humira was their biggest inflection point, and the basis on which they spun out of their parent company, Abbott Labs, back in 2013. Humira became the #1 best selling drug of all time in early 2013, surpassing Pfizer’s Lipitor after generic competition precipitated a 60% drop in its sales (1Q 2013 sales: $8.9 billion for Humira versus $3.6 billion Lipitor, a drop from $9 billion in the prior quarter). The reign of Humira lasted almost a decade, until Pfizer retook the crown with their COVID-19 vaccine Comirnaty (2Q 2021 sales: $20.3 billion for Humira versus $31.4 billion for Comirnaty). By targeting TNF-alpha, Humira created a pipeline-in-a-product that revolutionized rheumatology, dermatology, and gastroenterology. However, broad systemic inhibition acted like a blunt instrument, highly effective at dampening systemic inflammation, but frequently constrained by systemic side effects and ceiling effects in clear skin or mucosal healing. As Humira approached its own patent cliff in January 2023 (triggered by the launch of Amgen’s biosimilar Amjevita), AbbVie leveraged their decades of clinical insight to develop more targeted immunology medicines:

Skyrizi zeroed in on the p19 subunit of IL-23, cleanly shutting down the pathogenic Th17 pathway in psoriasis and IBD without touching the IL-12 pathway, thereby avoiding broad immune suppression.

Rinvoq moved intracellularly to selectively inhibit JAK1, providing a potent, rapid small-molecule alternative where broad biologics failed.

The increased specificity of these molecules yielded superior efficacy, allowing AbbVie to replace their own legacy asset with a dual-engine blockbuster portfolio.

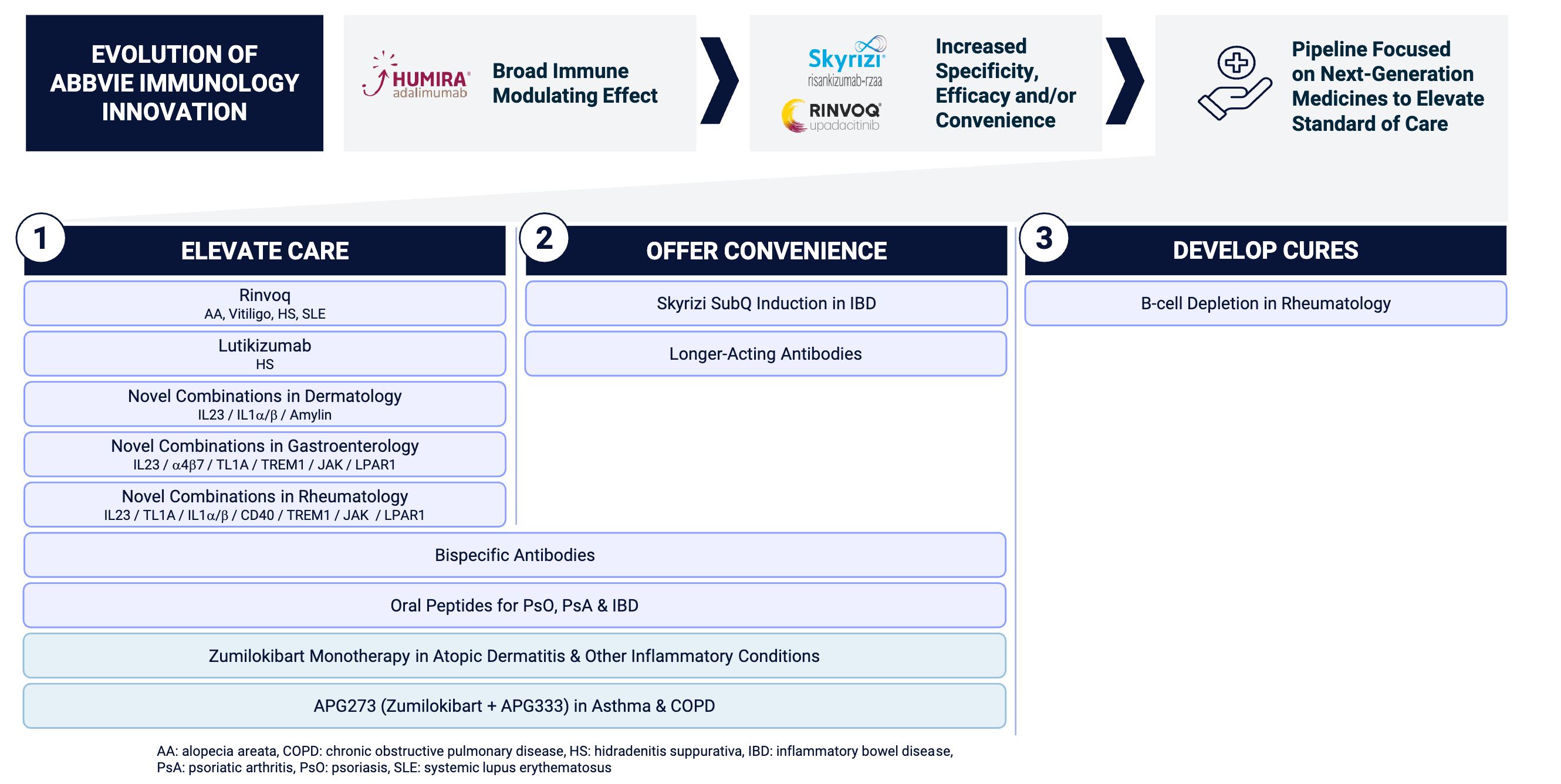

AbbVie’s current pipeline expansion, anchored by the Apogee acquisition, represents a third act. Their immunology strategy rests on three pillars:

Elevate Care: This strategic goal focuses on maximizing existing blockbusters through indication expansion and developing multi-targeting novel combinations to achieve deeper efficacy. Specific implementation includes expanding Rinvoq into new indications, advancing assets like lutikizumab for HS, and building combo regiments across dermatology, gastroenterology, and rheumatology.

Offer Convenience: AbbVie recognizes that long-term patient adherence and market dominance rely heavily on treatment convenience, ease of administration, and less frequent dosing. This is highlighted by the development of Skyrizi subcutaneous induction in IBD, which allows patients patients more manageable administration routes during the intense initial phases of treatment.

Develop Cures: The final, most ambitious pillar represents a shift from merely managing chronic inflammation to achieving profound, long-lasting disease modification or complete clinical remission. By targeting and deleting the specific B-cells driving autoimmune pathogenesis, AbbVie’s ultimate strategic goal under this pillar is to reset the immune system, moving closer to functional “cures” for severe rheumatological diseases.

The Apogee acquisition falls under the first two pillars (elevate care, offer convenience). By bringing in zumilokibart and its companion fixed-dose combinations (APG279 and APG273), AbbVie elevates care through multi-variant targeting, designed to simultaneously shut down downstream inflammation (IL-13) and upstream triggers (OX40L/TSLP) to bypass compensatory immune escape pathways and induce deeper clinical remissions. Crucially, these assets leverage advanced half-life extension technology, potentially offering unprecedented convenience in atopic dermatitis and allergy markets by shifting the standard of care from frequent bi-weekly injections to quarterly or twice-yearly maintenance dosing.

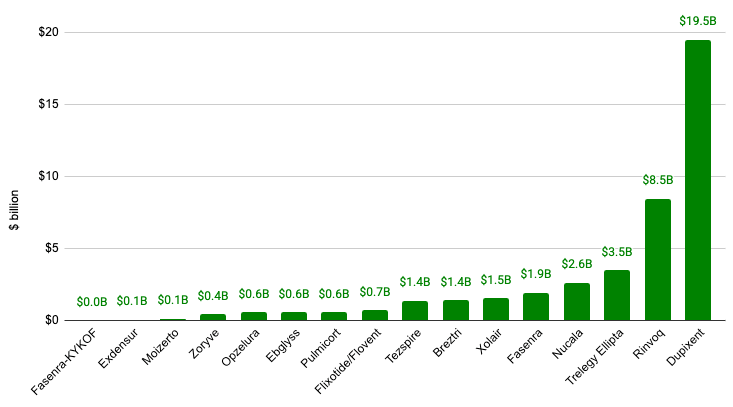

Atopic dermatitis and allergy markets are nothing to sneeze at. When combined, the commercial market for atopic dermatitis and allergy generates more than $43 billion every year and is growing at 28% annually, but market share is heavily concentrated at the very top. Sanofi/Regeneron’s Dupixent is the undisputed titan of this landscape, pulling in $19.5 billion on its own, accounting for nearly 45% of the entire listed market’s revenue. Rinvoq stands in second place at $8.5 billion. Combined, Dupixent and Rinvoq commands almost 65% of total sales among these leading brands, highlighting the massive commercial success of targeting Type 2 inflammation pathways (IL-4/IL-13) and JAK pathways in atopic dermatitis and severe asthma. Could Apogee be the key to claiming the top spot?

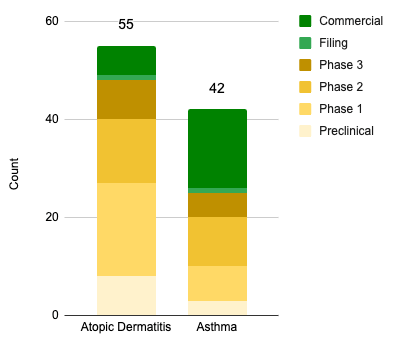

Atopic dermatitis and allergy spaces are very crowded, suggesting the highly selective nature of AbbVie’s purchase. Atopic dermatitis has the highest volume of active development (55 assets). The vast majority of its pipeline is concentrated in early-to-mid stage research (Phase 1 and Phase 2), indicating a massive wave of next-generation candidates working their way through clinical testing. There is also a notable block of Phase 3 assets preparing for market entry. While slightly smaller than the atopic dermatitis pipeline (42 assets), asthma boasts a highly robust clinical portfolio. Interestingly, a much larger proportion of the asthma pipeline is already sitting in the commercial category compared to atopic dermatitis, reflecting a mature biologic and triple-therapy marketplace that next-generation assets will have to disrupt. Standard me-too drugs could struggle in crowded markets like this. To win a share of this multi-billion dollar pie, next-generation drugs will likely need to offer clear points of differentiation. Apogee’s founding team baked in points of differentiation from the very start.

Entering the Fray

Apogee Therapeutics started as part of a hub-and-spoke biotech company, a corporate structure where a central parent organization (the hub) provides capital, operational infrastructure, and shared expertise to incubate and manage a portfolio of distinct, specialized subsidiary companies (the spokes). We’ve discussed this corporate structure before (Incyte to Acquire Vega). It enables companies to develop a medicine in a more capital efficient way and sell it without giving up the rest of the pipeline. In less than four years, Apogee went from an incubation concept to a multi-billion-dollar market leader, culminating in its acquisition.

In 2021, the investment firm Fairmount Funds launched Paragon Therapeutics (the hub) to serve as a high-efficiency antibody discovery engine. Apogee Therapeutics (a spoke) was built to solve a specific problem: navigating crowded immunology markets by utilizing superior antibody engineering rather than completely unproven biology. Founded by Fairmount and Venrock, Apogee officially launched in December 2022 as the very first spinout company from Paragon. Led by CEO Michael Henderson, Apogee secured exclusive development and commercial rights to a suite of pre-optimized, half-life-extended antibodies discovered by Paragon. The company emerged from stealth with a total of $169 million across Series A and B rounds, with the latter round adding Deep Track Capital and RTW Investments to the cap table.

Instead of spending years in early preclinical phases, Apogee moved at an extraordinary pace due to the high-throughput engineering foundation inherited from Paragon. Just seven months after emerging from stealth, Apogee went public on the Nasdaq. Despite a relatively cold market for biotech IPOs at the time, investor enthusiasm for their extended half-life value proposition allowed Apogee to raise $300 million. In March 2024, Apogee announced highly anticipated Phase 1 clinical data for its lead asset, APG777 (zumilokibart). The trial demonstrated that zumilokibart possessed an unprecedented 75-day half-life, roughly 3 to 4 times longer than existing IL-13 competitors like lebrikizumab. This readout confirmed that Apogee’s half-life extension thesis translated to humans.

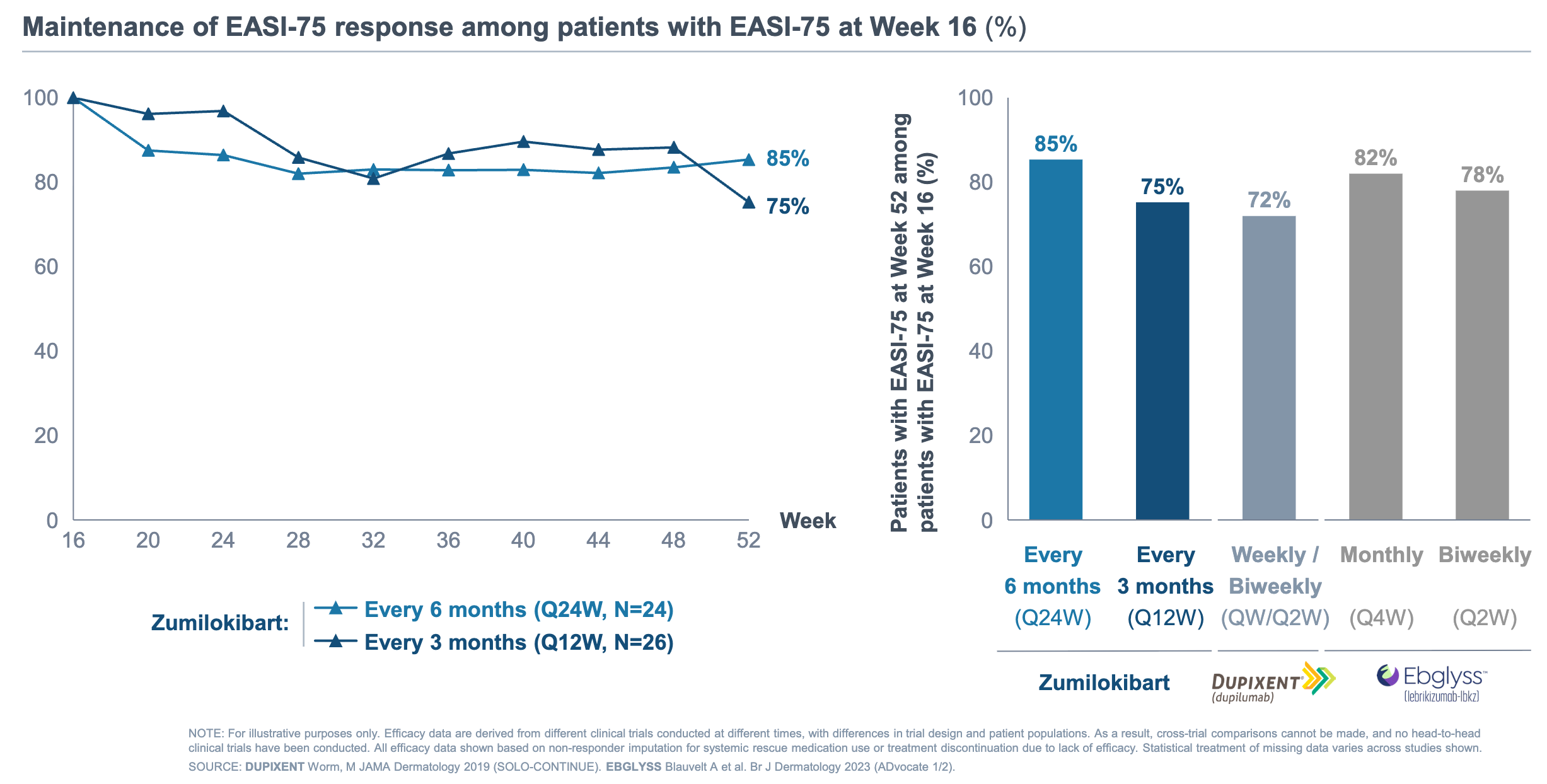

Over the next two years, the company executed a tightly coordinated clinical program designed to uncover zumilokibart’s efficacy profile. In March 2026, Apogee took a direct shot at the market’s heavy hitters by reporting long-term 52-week data from Part A of its Phase 2 APEX trial in moderate-to-severe atopic dermatitis. While current biologics require bi-weekly or monthly maintenance injections, Apogee evaluated maintenance dosing intervals stretching to every 3 and 6 months. Among patients who initially responded at Week 16, 75% of those on the 3-month regimen and 85% on the 6-month regimen successfully maintained their EASI-75 response out to one full year. This data appears competitive with commercial anti-IL13 mAbs on a cross-trial basis.

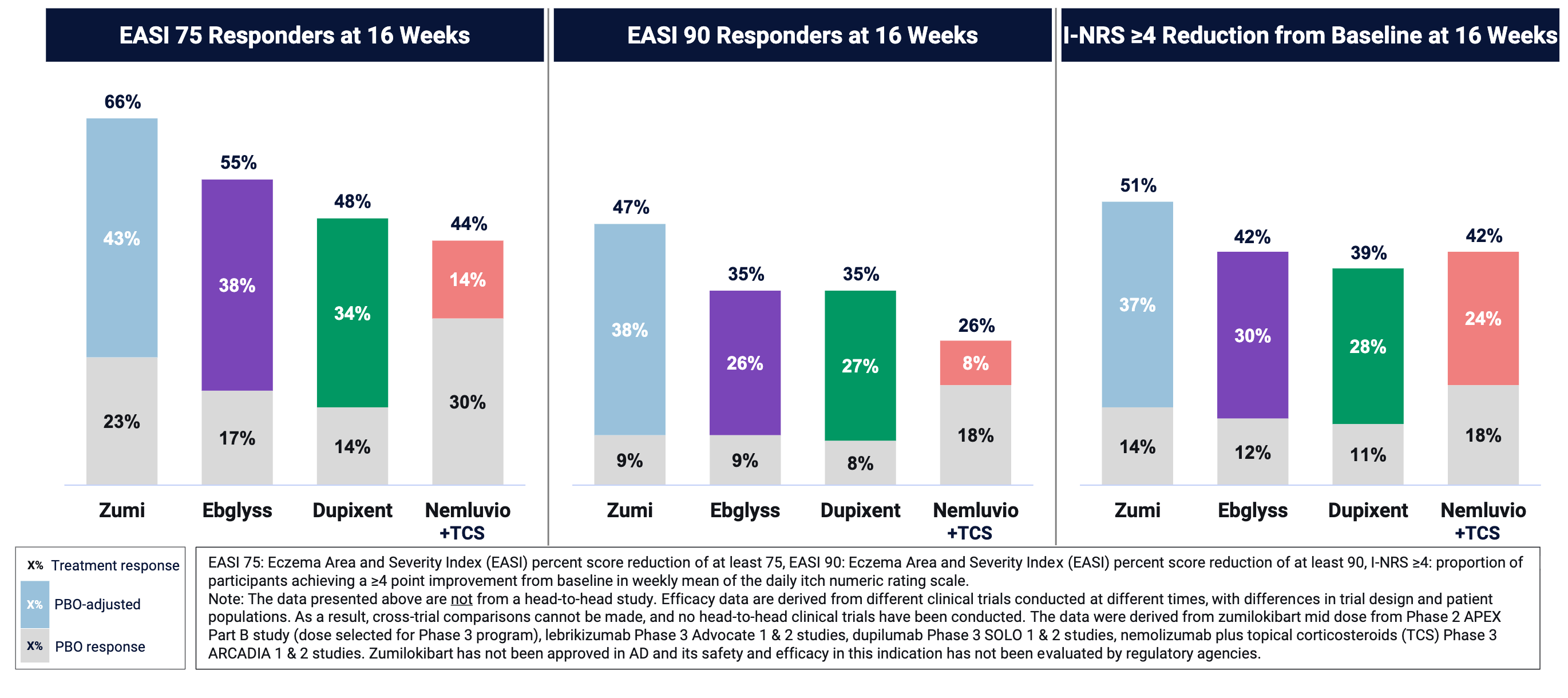

A mere two months later, in May 2026, Apogee closed the loop on its Phase 2 program by presenting the 16-week Part B induction dose optimization data. Enrolling 346 adult patients across low, mid, and high doses against placebo, the trial established the mid-dose as a formidable winner. Nearly two-thirds of patients (66%) achieved EASI-75 at week 16, accompanied by robust skin clearance (47% achieving IGA 0/1) and rapid itch relief. With the asset demonstrating a safety profile that was generally well-tolerated and entirely in line with the class, Part B gave Apogee the information required to lock in its Phase 3 protocol.

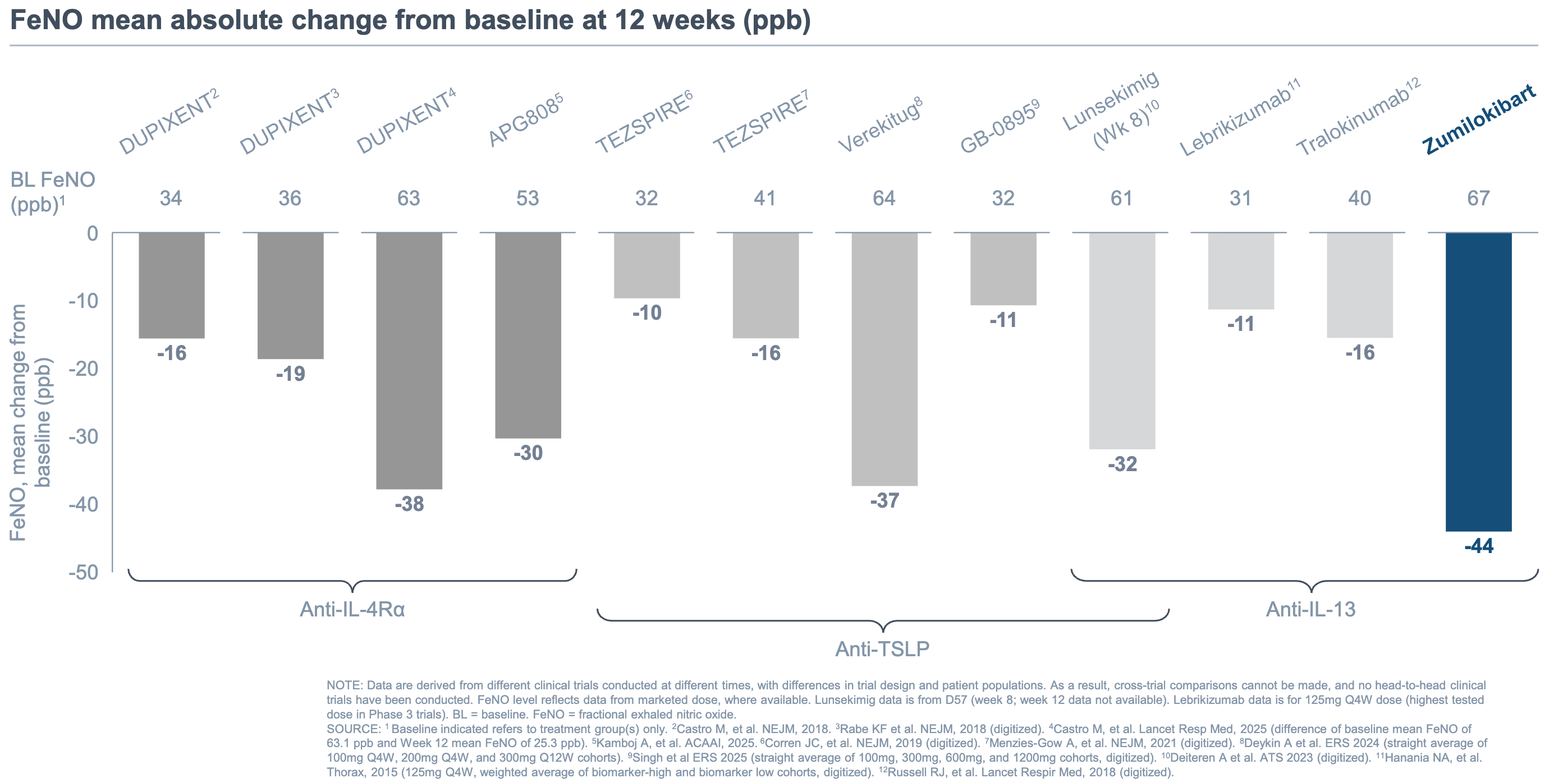

While cementing its position in dermatology, Apogee simultaneously expanded zumilokibart’s footprint into respiratory medicine. In January 2026, the company announced positive proof-of-concept interim results from a Phase 1b trial in mild-to-moderate asthma, confirming that the asset’s tissue penetration and biomarker suppression mirrored its dermatological success. Zumilokibart established a competitive profile in suppressing fractional exhaled nitric oxide (FeNO), a crucial biomarker of Type 2 airway inflammation, when evaluated alongside leading and emerging asthma therapies at the 12-week mark. While the cross-trial comparison below differs in trial design and patient baselines, the data paints a compelling narrative for zumilokibart’s best-in-class potential in asthma.

Concurrently, the foundational single-agent components of Apogee’s multiplexed combinations were validated. APG333 (the anti-TSLP arm of the APG273 combination) completed its own Phase 1 trial, matching zumilokibart’s extended kinetics and demonstrating competitive Type 2 inflammatory biomarker suppression for up to six months from a single dose. This paved a clinical path for late-2026 combination trials in asthma and COPD.

By mid-2026, Apogee’s clinical momentum had caught the attention of an industry titan managing its own immunology legacy, AbbVie. Armed with clean 52-week maintenance data, optimized Phase 3-ready dosing, an expanded Phase 1b head-to-head trial of APG279 versus Dupixent, and a pristine cash position of $1.3 billion, Apogee reached its ultimate destination. On June 22, 2026, AbbVie announced a definitive agreement to acquire Apogee for $10.9 billion in cash, bringing this chapter of rapid clinical execution to a historic, mega-blockbuster conclusion.

Conclusion

AbbVie’s $10.9 billion acquisition of Apogee Therapeutics represents a masterclass in strategic execution from both sides:

For AbbVie: It secures a powerful third act to succeed the Humira era and complement Skyrizi and Rinvoq. The potential to shift the standard of care from bi-weekly maintenance injections to a quarterly or twice-yearly schedule gives them an unmatched weapon in convenience to challenge Sanofi/Regeneron’s dominant Dupixent.

For Apogee: It stands as a flawless validation of the hub-and-spoke biotech model. Moving from stealth incubation to a historic $10.9 billion mega-blockbuster exit in under four years proves that combining highly efficient antibody engineering with hyper-accelerated clinical execution can disrupt even the most crowded therapeutic landscapes.

As these next-generation assets head into Phase 3 trials and direct head-to-head readouts later this year, the spotlight shifts to how quickly AbbVie can scale this pipeline. The race for dominance in the $43+ billion atopic dermatitis and allergy markets is heating up, and AbbVie has a hot hand.

Love biotech? Check out Biotech Readout’s full content library, or navigate directly to a segment that interests you:

Frontiers in Medicine: Exploring the frontiers of our understanding and treatments for disease.

Medical History: Recovering forgotten relics in the history of medicine.

Acquisitions: Exploring the innovation behind acquired companies.

Weekly Readout: A digest of new clinical data from the past week.

To contact us, please send us an email at biotechreadout@gmail.com

Disclaimers

Investigational Status Disclaimer

The therapeutic candidates discussed in this newsletter are currently in clinical development and have not been approved for commercial sale by the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), or other global regulatory authorities. Their safety and efficacy have not been established. References to pipeline products and ongoing clinical trials involve significant risks and uncertainties. Statements regarding the potential safety, potency, or efficacy of investigational drugs reflect current hypotheses and are not a guarantee of future performance or regulatory clearance. The outcome of clinical trials is inherently unpredictable, and clinical results from earlier stages may not be predictive of results in later, larger-scale trials.

No Medical Advice Disclaimer

This newsletter is for informational and educational purposes only. The content is not intended to be a substitute for professional medical advice, diagnosis, or treatment. Always seek the advice of your physician or another qualified health provider with any questions you may have regarding a medical condition. Never disregard professional medical advice or delay in seeking it because of something you have read in this publication.

No Patient-Provider Relationship Disclaimer

The information provided in this newsletter is for educational and analytical purposes only. Receipt of this information, or any interaction with this content, does not create a physician-patient, pharmacist-patient, or any other professional-provider relationship between you and the authors or publishers. This newsletter should not be used as a substitute for a personal consultation with a qualified healthcare professional.

Forward-Looking Statements Disclaimer

This newsletter contains “forward-looking statements” regarding future events, including clinical trial timing, regulatory milestones, and projected market performance. These statements are based on current expectations and assumptions that are subject to significant risks and uncertainties. Actual results may differ materially from those expressed or implied. We undertake no obligation to update these statements as a result of new information or future developments.

Third-Party Links & Content Disclaimer

This newsletter contains links to third-party websites, including clinical trial registries and corporate presentations. Biotech Readout does not endorse, guarantee, or assume responsibility for the accuracy or reliability of any information offered by third-party providers.

Errors and Omissions Disclaimer

While we strive for technical accuracy, the information in this newsletter is provided on an “as is” basis with no guarantees of completeness, accuracy, or timeliness. Biotech Readout assumes no liability for any errors or omissions in the content of this publication.

Non-Endorsement Disclaimer

Any reference to specific commercial products, processes, or services by trade name, trademark, or manufacturer does not constitute or imply an endorsement or recommendation by the author. All trademarks are the property of their respective owners.

No Investment Advice Disclaimer

This newsletter is for informational purposes only and does not constitute financial, investment, or legal advice. The author is not a registered investment advisor. You should consult with a professional financial advisor before making any investment decisions. The biotechnology sector is highly volatile; past performance is not indicative of future results.

Conflict of Interest Disclaimer

The author of this newsletter maintains a position of independence. At the time of publication, the author holds no direct financial interest, equity, or options in any of the companies mentioned in this report. No compensation has been received from any third party to feature or analyze specific therapeutic candidates or corporate entities.