Vertex to Acquire Crinetics

How R. Scott Struthers and his crew from Neurocrine went out on their own and struck gold in rare metabolic disease

Disclaimer: This newsletter is for educational and informational purposes only and does not constitute medical, investment, or financial advice, nor does it establish a provider-patient relationship. Content may include forward-looking statements and discussions of investigational therapeutic candidates that are not FDA/EMA approved; their safety and efficacy remain unestablished and clinical outcomes are unpredictable. While we strive for accuracy, all information is provided as is without guarantees. As of the date of publication, the author holds no direct equity positions in the specific companies mentioned in this issue nor receives third-party compensation for this coverage. Please find a complete version of our disclaimers linked here.

If you are a paid subscriber, go to this article’s premium charts & analysis here ⬇️

If you are a free reader or subscriber, enjoy the whole article free of charge and consider upgrading for premium charts & analysis on acromegaly and CAH.

Introduction

On July 6, 2026, Vertex Pharmaceuticals Incorporated announced a definitive agreement to acquire Crinetics Pharmaceuticals, Inc. for a total equity value of approximately $10.0 billion (Vertex press release, Vertex slide deck, Crinetics press release). This acquisition centers on the two most advanced programs in Crinetics’ pipeline:

Palsonify (paltusotine; FDA-approved SST2 agonist): In September 2025, the FDA approved this drug for the treatment of adults with acromegaly who have had an inadequate response to surgery and/or who are not candidates for surgery. It is also being investigated in Phase 3 trials for carcinoid syndrome associated with neuroendocrine tumors (NETs). Palsonify is the first once-daily oral small molecule to achieve FDA approval in acromegaly, providing patients with a non-invasive alternative that maintains biochemical control (normalization of IGF-1 and growth hormone levels).

Atumelnant (ACTH inhibitor in Phase 3): This is an investigational agent currently in Phase 3 development (CALM-CAH trial). It is being developed for ACTH-dependent endocrine disorders, primarily Classic Congenital Adrenal Hyperplasia (CAH) and ACTH-dependent Cushing’s Syndrome (ADCS).

In this article, we tease out Vertex’s M&A strategy, learn how a team of Neurocrine scientists struck out on their own to start Crinetics, and do a deep pull of their under-discussed early stage pipeline.

A Peek Into Vertex’s M&A Strategy

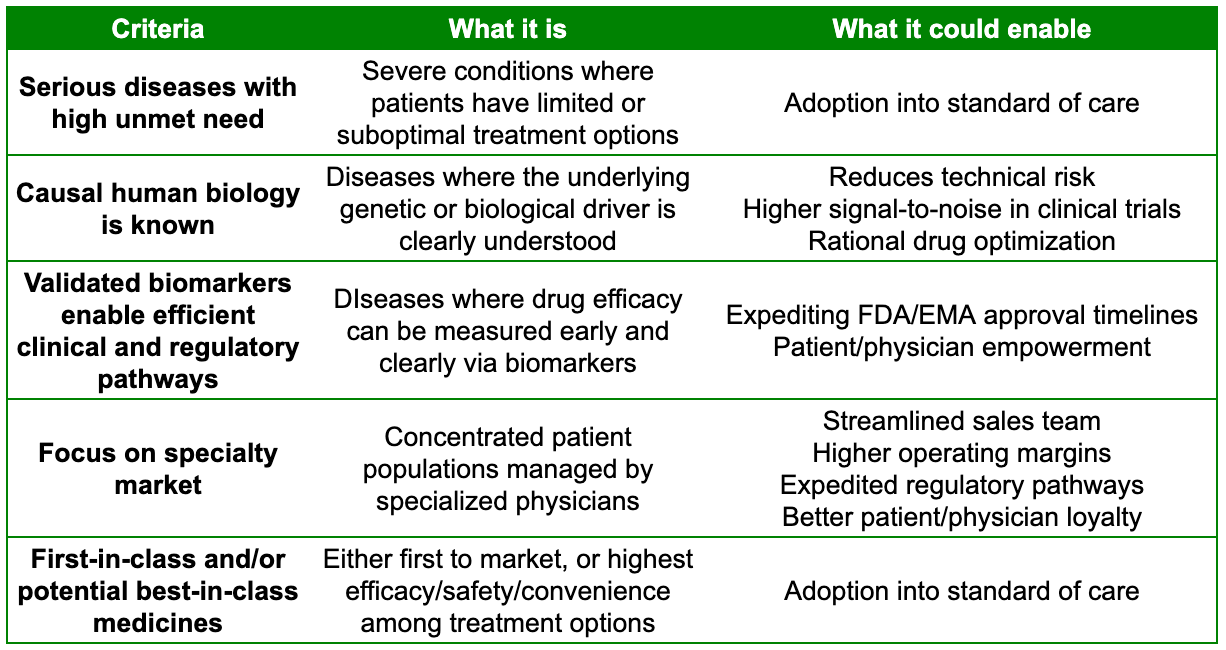

During Vertex’s presentation regarding its $10 billion acquisition of Crinetics, CEO Reshma Kewalramani outlined a set of five criteria that the company looks for in order to gauge strategic fit, noting that she viewed both Palsonify and atumelnant as meeting all of them:

Together, Vertex contends that these five criteria act as a flywheel. Since they target specialty markets, they require limited SG&A (Sales, General & Administrative) expenses and infrastructure to market a drug. High-value transformative medicines command strong pricing power, leading to robust operating margins and significant cash flow. In other words, they follow the old adage of ‘doing well by doing good’. Vertex can then use that cash flow to invest the heavy majority of its operating expenses right back into internal R&D and external innovation to create new high-impact medicines, repeating the cycle.

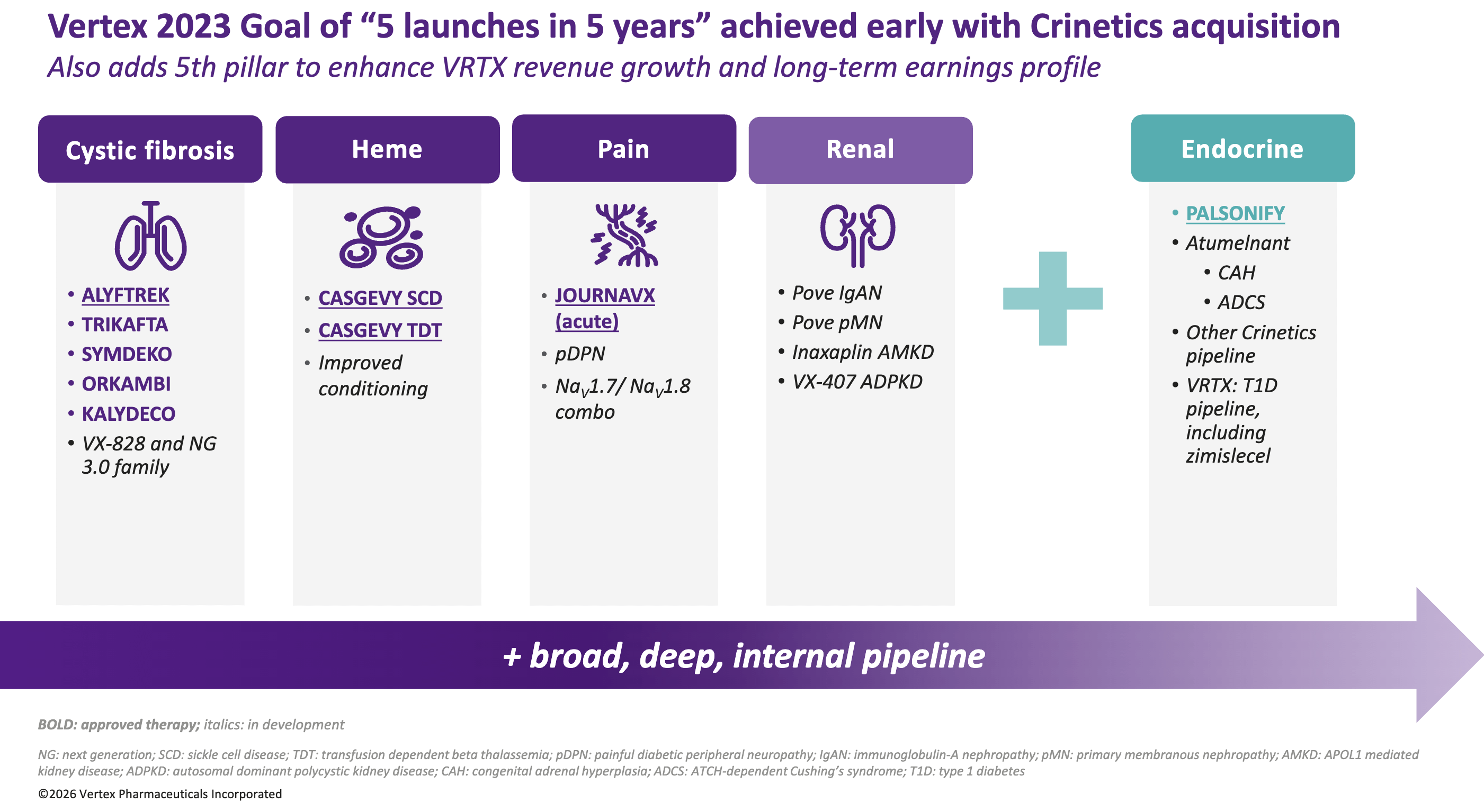

Separately, Vertex originally set an ambitious internal goal in 2023 to launch 5 new medicines within 5 years. By acquiring Crinetics, which features the recently approved Palsonify and late-stage atumelnant, Vertex successfully checked off this strategic milestone more than two years ahead of its deadline and added a new vertical to their rare disease pipeline (see below). By acquiring a company with an existing commercial footprint (Palsonify) alongside a deep, mid-to-late-stage pipeline (atumelnant and others), Vertex aims to establish a scaled endocrinology franchise while building a potential runway for long-term growth.

Self-made Scientists

The pioneers of Silicon Valley’s technology boom are known as the “Traitorous Eight”, a group of eight employees who resigned from Shockley Semiconductor Laboratory in 1957 due to William Shockley’s authoritarian management and research direction to found Fairchild Semiconductor. Fairchild went on to invent the first commercially viable integrated circuit and members of this group spun out to found Intel, AMD, and some of the world’s largest venture capital firms (like Kleiner Perkins). The story of Crinetics starts less than 500 miles away in San Diego, and echoes the courageous founding story of Fairchild.

In May 2006, the FDA issued a crushing complete response letter (CRL) to Neurocrine Biosciences for indiplon, an experimental insomnia drug partnered with Pfizer in a deal worth up to $400 million, requesting an immediate-release version of the modified-release version. Pfizer immediately terminated the partnership, stripping Neurocrine of its primary funding engine. When a 2007 resubmission resulted in yet another CRL demanding costly new clinical safety studies, Neurocrine was forced to completely abandon the drug in the U.S. With its primary asset dead and its stock price tumbling, Neurocrine had to execute a brutal pivot to stabilize the business. Gary Lyons, who had served as CEO and President since the company’s founding in 1993, stepped down in January 2008. He was replaced by Dr. Kevin Gorman, who was tasked with completely re-architecting the company’s survival strategy. Neurocrine underwent consecutive rounds of workforce restructuring. In a short period, the company slashed its workforce from hundreds of employees down to a lean core of just about 60 people.

Neurocrine also decided to pool their remaining capital into just two high-value clinical assets, which they deemed to have the highest probability of success (what eventually became Orlissa for endometriosis & uterine fibroids and Ingrezza for tardive dyskinesia). This aggressive funneling of resources meant that excellent internal programs deemed “non-essential” for Neurocrine’s immediate survival were abruptly shelved or de-prioritized. Among these hidden gems was a deep, world-class exploratory research platform focused on peptide chemistry and G-protein coupled receptors (GPCRs) in endocrinology which included a team composed of Dr. R. Scott Struthers, Dr. Stephen Betz, Dr. Frank Zhu, and Dr. Ana Kusnetzow. Dr. R. Scott Struthers and his core team of fellow Neurocrine scientists knew this platform possessed immense therapeutic potential, particularly for rare endocrine diseases like acromegaly. However, they also recognized that Neurocrine, in its newly restructured state, could no longer fund broad, early-stage endocrine discovery.

Rather than letting decades of collective expertise evaporate in the layoffs, Struthers and his colleagues parted ways with the parent company in 2008 to form Crinetics Pharmaceuticals. By breaking away, they preserved that specialized GPCR chemistry engine, carrying forward a scientific torch that Neurocrine was forced to drop. They did not have millions in initial venture funding. Instead, they bootstrapped the early years through highly competitive NIH grants and peer-validated non-dilutive funding, focusing their brilliant chemical design engines on the human endocrine system. Endocrinology was historically dominated by large pharma companies manufacturing injectable peptide biologics. For rare endocrine diseases like acromegaly (severe overgrowth of bones and organs caused by excess growth hormone), the standard of care was burdensome: patients had to visit clinics for painful, large-needle, deep intramuscular or subcutaneous injections every month. The Crinetics founders asked a simple question: What if we could design an oral, once-daily non-peptide small molecule that binds to the same receptors just as powerfully?

In 2016, after years of iterative synthesis, the team crossed an early checkpoint. They synthesized a molecule called paltusotine (originally CRN00808). It was a selective, non-peptide oral somatostatin receptor type 2 (SST2) agonist designed to shut down excess growth hormone. Since it was a pill, it eliminated the need for a needle. Backed by this stellar chemistry, blue-chip healthcare venture firms like 5AM Ventures and OrbiMed took notice, infusing the company with the capital required to enter the clinic. To fund expensive late-stage clinical trials, Crinetics went public on the NASDAQ exchange in 2018.

Over the next several years, under the steady leadership of CEO Scott Struthers, the company transitioned from a lean discovery shop into a clinical execution powerhouse. They deliberately avoided diversifying into completely unrelated therapeutic areas, choosing instead to double down on endocrinology. They uncovered a second pipeline asset: atumelnant (CRN04894), the first oral, once-daily ACTH receptor antagonist designed to treat grueling conditions like Congenital Adrenal Hyperplasia (CAH) and Cushing’s syndrome.

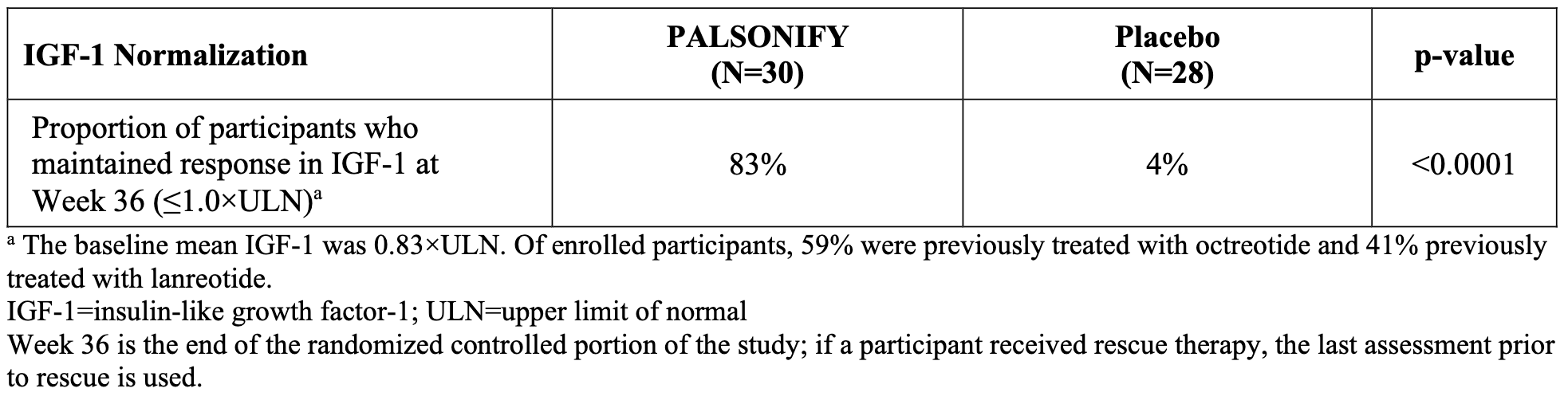

A major inflection point arrived between 2023 and 2024 when Crinetics announced resounding success in its Phase 3 PATHFNDR trials for paltusotine. The data proved that a single daily pill could maintain disease control and suppress symptoms just as effectively as the painful, deep-tissue legacy injections. The first trial (PATHFNDR-1) addressed the hundreds of thousands of acromegaly patients worldwide already stabilized on standard-of-care monthly injectable somatostatin receptor ligands (SRLs) like octreotide or lanreotide. These patients were forced to endure deep, painful tissue injections that often left behind bruising, nodules, and breakthrough symptoms as the month waned. The trial showed that a stunning 83% of patients on paltusotine successfully maintained their IGF-1 levels at or below the upper limit of normal (≤1x ULN), compared to a dismal 4% of patients randomized to the placebo group who saw their disease biomarkers spike almost immediately after stopping their injections.

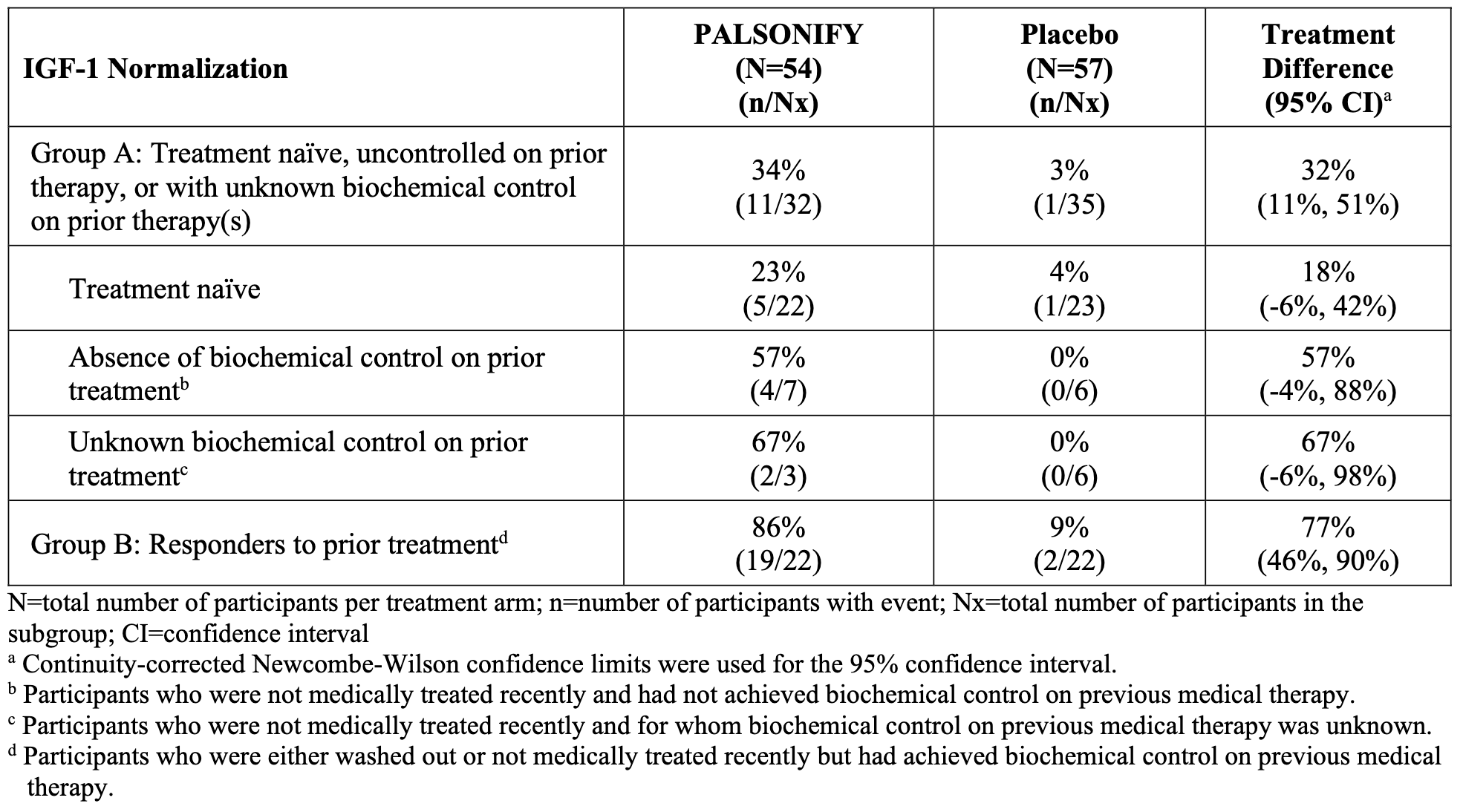

With PATHFNDR-1 proving that controlled patients could be safely transitioned onto paltusotine, Crinetics launched its second major front: PATHFNDR-2. This trial was designed to test the drug’s potency in sicker patients who had active, biochemically uncontrolled acromegaly. The trial enrolled 111 adult patients who were either entirely medication-naïve (had never received medical therapy after an unsuccessful surgery) or had completely washed out of prior medications, entering the trial with highly elevated, active baseline IGF-1 levels. By the end of the 24-week randomized control period, 55.6% of paltusotine-treated patients achieved complete biochemical normalization (≤1x ULN), obliterating the 5.3% response rate in the placebo arm (P < 0.0001). The majority of participants who achieved IGF-1 normalization during the trial did so within the first 2-4 weeks following initiation of treatment, with sustained response through the end of the treatment period. A posthoc subgroup analysis clarified the response rates in patient subpopulations with different disease severity (ie. better or worse responses to prior therapy), shown in the table below.

Crucially, across both trials, the safety profile remained relatively clean. There were no serious adverse events attributed to paltusotine during the randomized control phases. The only side effects noted were mild, transient gastrointestinal shifts (like mild diarrhea or abdominal discomfort) typically observed with any somatostatin-class medicine, which quickly resolved without forcing discontinuation. The final validation of the PATHFNDR program came from its Open-Label Extensions (OLE) data, which was presented at ENDO 2026. When given the choice at the end of the blind trials, an overwhelming majority of patients (93% from PATHFNDR-1 and over 97% from PATHFNDR-2) actively refused to go back to legacy monthly injections, choosing instead to enroll in the long-term oral tracking study. Long-term data tracking these extension cohorts out for a full two years confirmed that the oral drug’s efficacy never waned, maintaining stable biomarker and symptom control across the board.

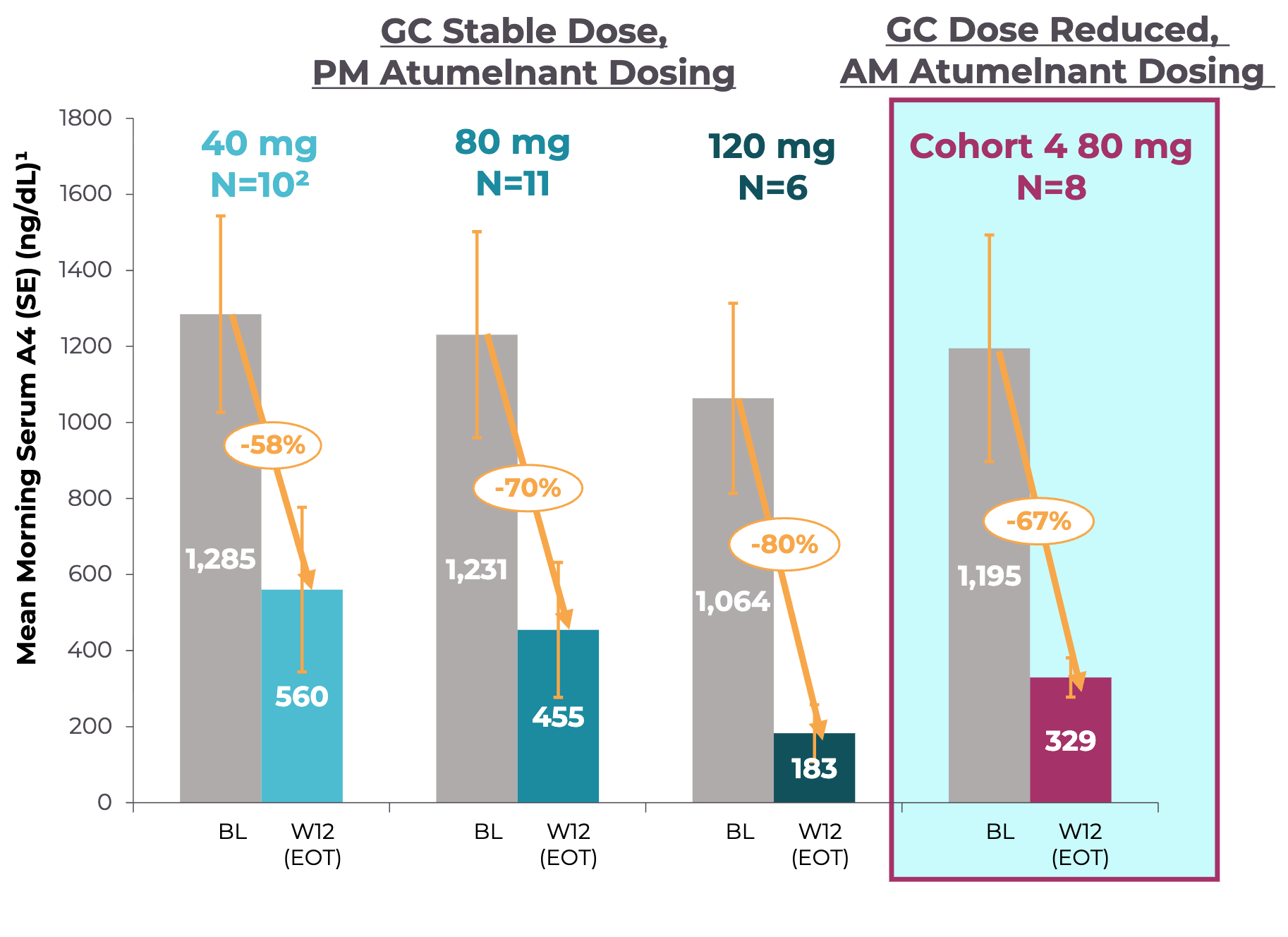

Shortly after Palsonify’s topline Phase 3 success, Crinetics’ second program atumelnant posted stellar Phase 2 results. Historically, CAH patients have had to take massive, supraphysiologic doses of glucocorticoids just to suppress excess adrenal androgens, resulting in severe steroid-induced side effects like weight gain, diabetes, and osteoporosis. As a first-in-class, once-daily oral ACTH receptor antagonist, Atumelnant aimed to bypass this entire cycle by directly blocking androgens production in the adrenal cortex. In the Cohort 4 of atumelnant’s Phase 2 trial, the drug maintained a -67% mean reduction in A4 morning serum levels at week 12 (see graph below). This reduction was observed despite the trial’s strict protocol of titrating patients off their high-dose steroid regimens down to safe, physiologic replacement levels (i.e. removing background treatment). Furthermore, 88% of patients in the trial (7 out of 8) successfully transitioned down to physiologic daily doses of glucocorticoids without losing control of their androgens. These data suggest the potential to decouple the management of hyperandrogenism from high-dose steroid toxicity. Across all cohorts and extending into the Open-Label Extension (OLE) representing hundreds of cumulative weeks of exposure, atumelnant proved to be generally well-tolerated. There were zero treatment-related severe or serious adverse events (SAEs), no patients dropped out of the study due to drug tolerability issues, and there were no hepatic transaminase or liver-related adverse events. The most common mild side effects recorded were simple headaches and fatigue. The adult Phase 3 clinical development program evaluating atumelnant (CALM-CAH trial) officially began in late 2025. Shortly thereafter, in January 2026, Crinetics expanded the Phase 3 clinical footprint by initiating a separate pediatric Phase 2/3 trial (the Balance-CAH study) to evaluate the drug’s efficacy and safety in children and adolescents living with classic CAH.

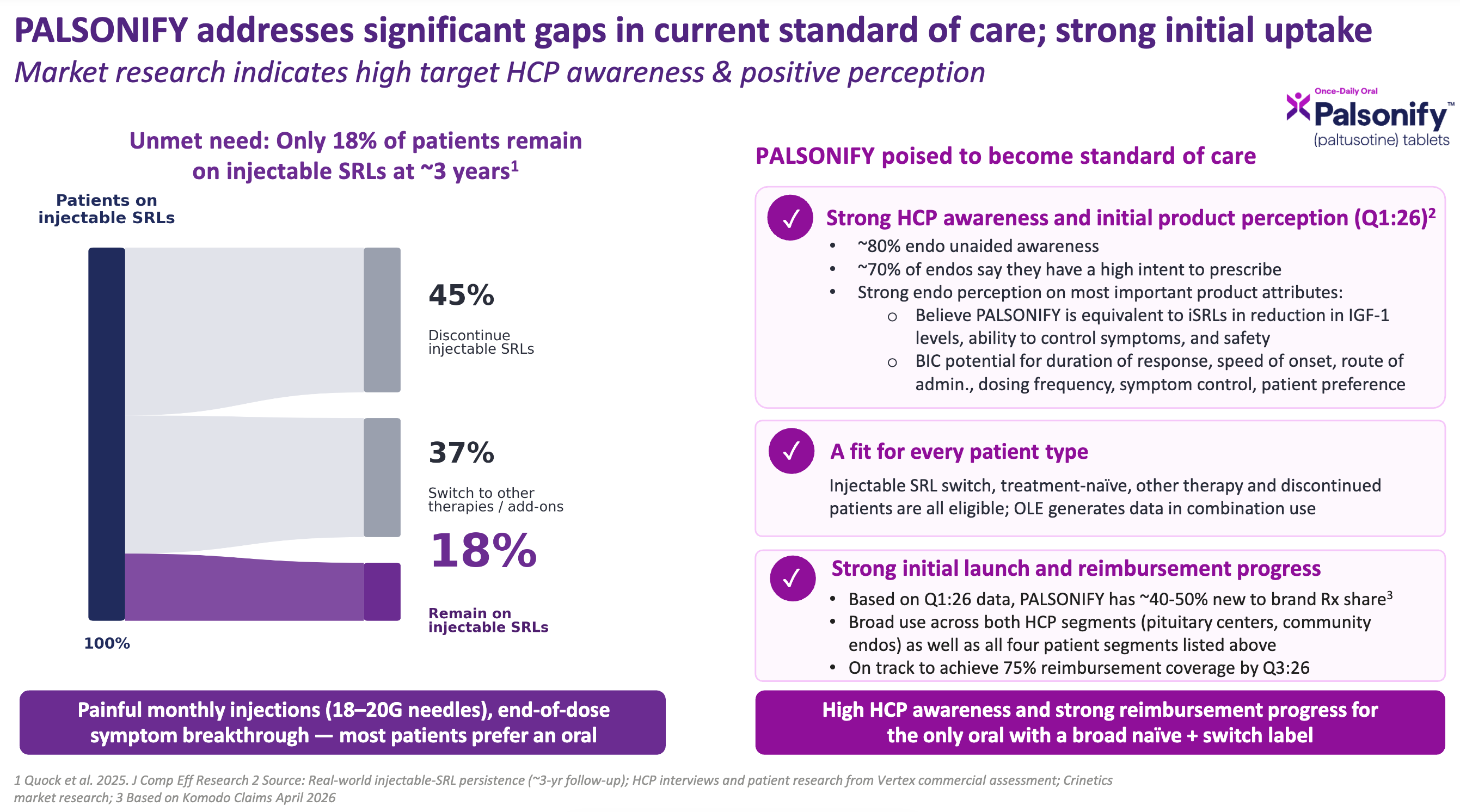

In September 2025, the FDA officially approved paltusotine under the brand name Palsonify. It made medical history as the first and only once-daily oral alternative to injectable therapies for adults living with acromegaly. Soon after, the European Medicines Agency (EMA) followed suit with its own approval. Crinetics immediately began setting up commercial infrastructure and gaining early momentum. For a drug that only recently launched, the awareness and intent among endocrinologists was exceptionally mature, as captured in Vertex’s market research (see below).

Among potential prescribing doctors (endocrinologists):

About 80% of doctors already knew Palsonify by name without being prompted, indicating highly effective scientific communication and medical affairs execution.

About 70% of doctors were actively prepared to write prescriptions for Palsonify.

Endocrinologists viewed Palsonify as equal to injectables in raw efficacy, but viewed it as a best-in-class (BIC) option across patient preference metrics: speed of onset, oral route of administration, once-daily dosing frequency, and duration of response.

In rare disease launches, commercial uptake is often throttled because a drug is only approved for a very narrow subset of patients (e.g., only those who fail surgery). Palsonify avoids this trap with a broad label covering both treatment-naïve patients and those switching from other therapies. Whether a patient is an injectable switch, completely treatment-naïve, on another add-on therapy, or one of the 45% who discontinued prior treatment entirely, they are all eligible. In its very first few months on the market, Palsonify has already captured up to half (40-50%) of all newly initiated or switched prescriptions in the space, according to Vertex’s Komodo Claims Analysis from April 2026. The biggest barrier to any biotech launch is getting insurance companies to pay for it. Palsonify is on an accelerated trajectory, on track to achieve 75% reimbursement coverage by the third quarter of 2026, according to Vertex. With half of the new prescription market share already captured, near-total physician awareness, and broad insurance coverage locking in by next quarter, Palsonify’s appears to be rapidly solidifying its place as the new standard of care for acromegaly.

Recognizing that Crinetics matched Vertex’s acquisition criteria for high-margin, low-overhead specialty assets, the biotech titan stepped in. On July 6, 2026, Vertex announced a definitive agreement to acquire Crinetics for approximately $10.0 billion. Reflecting on the monumental decades-long journey from a modest startup to a multi-billion dollar cornerstone of Vertex’s new endocrinology disease pillar, Dr. Scott Struthers remarked, “Nearly 18 years ago, we founded Crinetics with a clear goal of transforming the lives of patients living with endocrine-related diseases. Today marks a historic milestone as we embark on this next chapter with Vertex.”

Excavating Crinetics’ Hidden Gems

During Vertex’s presentation, Charles Wagner (EVP, COO and CFO at Vertex) briefly commented, “We also see value in Crinetics additional pipeline assets. We’ll discuss that post close [of the acquisition].” Well, consider this an unofficial preview, courtesy of Biotech Readout. I noticed that the Crinetics pipeline is much larger than the two programs headlining the acquisition announcement. These assets are not the typical long tail of low-priority programs or backup molecules for lead programs. These assets aim to pursue large metabolic indications and even introduce a whole new drug modality. I’ll start with the latter.

CRN09682 is a first-in-class non-Peptide Drug Conjugate (NDC), a spin on the antibody-drug conjugate (ADC) but with a small molecule for targeting instead of an antibody. It consists of a selective, small-molecule SST2 agonist chemically linked to a potent cytotoxic payload, monomethyl auristatin E (MMAE), via a spacer and a cleavable linker. Since small molecules exhibit distinct tissue penetration, stability, and clearance kinetics compared to large antibodies or peptides, this approach aims to deliver targeted cytotoxic agents deep into solid tumors with a shorter plasma half-life. The drug is being evaluated as a treatment for advanced, progressive metastatic, or locally inoperable neuroendocrine tumors (NETs), neuroendocrine carcinomas (NECs), and other solid tumors (e.g., small cell lung cancer, thyroid cancer, meningioma) that explicitly express somatostatin receptor type 2 (SST2). CRN09682 is in Phase 1/2 clinical development (the BRAVESST2 trial).

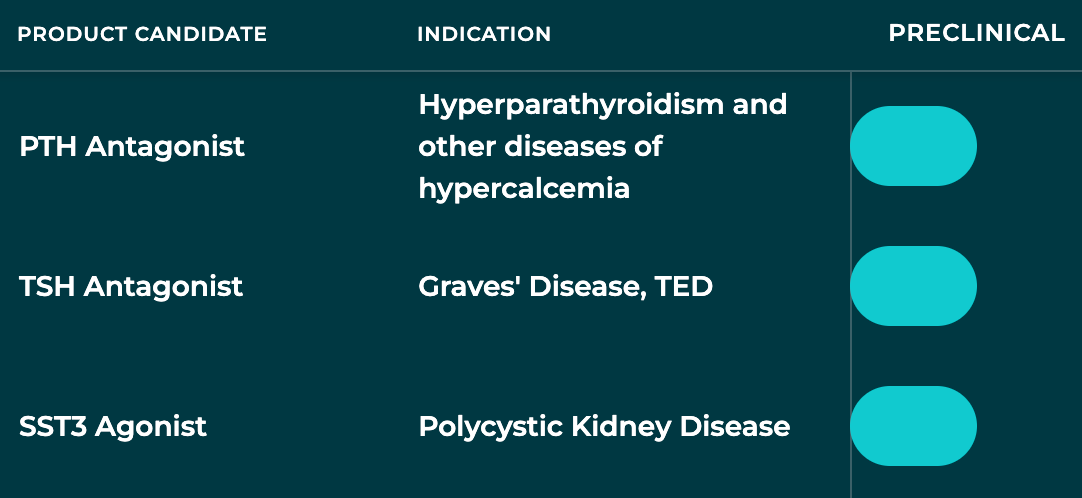

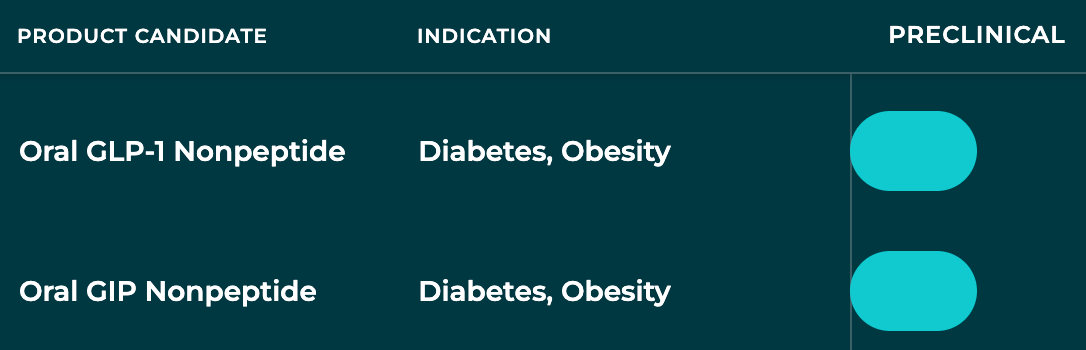

Okay, that’s intriguing. What else? How about once-daily oral small molecules for three large metabolic diseases that are currently dominated by injectables. So, I guess they were just getting warmed up with Palsonify.

But, wait there’s more. Hold on, I can’t quite make out the last two programs. Zoom and enhance that image.

Oh, it’s nothing; just two shots on goal for obesity, the largest drug market of all time. No wonder Vertex CEO Reshma Kewalramani spent so much time talking about the people and culture that they will gain by in-housing Crinetics. Clearly, the team has been hard at work creating expansive optionality for a cash-rich Vertex to potentially expand into a thriving ecosystem of franchises. I, for one, am very curious to hear what the Vertex team has to “discuss post close”.

Conclusion

The $10 billion acquisition of Crinetics is a testament to what happens when elite drug hunters double down on a scientific thesis. By transforming complex, burdensome peptide injections into elegant, once-daily oral therapies, R. Scott Struthers and his team are on track to redefine the standard of care for patients living with acromegaly and, perhaps someday, other rare metabolic diseases. As Crinetics integrates into the Vertex engine, the immediate commercial momentum of Palsonify and the potential of atumelnant are encouraging. But for long-term watchdogs, Crinetics’ early-stage pipeline could significantly sweeten the deal. If the Crinetics team can replicate their small-molecule magic in other markets like obesity and rare metabolic disease, Vertex’s ten-billion-dollar bet could look like the bargain of the decade.

Premium Charts & Analysis

All charts reflect data current as of the specified date and may not include every drug development program, although we aimed to capture the vast majority. Please feel free to email me at biotechreadout@gmail.com with “CHARTS” in the subject line to share suggestions or request chart updates.

Press ⬇️ to navigate to a section